by Derek Sheehan

Montana’s housing market in 2024 represents cooler weather in an enduring hot climate. The continuation of high interest rates chilled the pace of transactions on both sides of the market. Despite the cooling, Montana continues to be ranked at the bottom for affordability. Explaining much of the affordability issue is the fact that the state also ranks in the bottom third for median household incomes. While this would typically place downward pressure on the cost of housing, there are longer-term trends that keep the market warm.

These affordability challenges are compounded by longer-term U.S. migration trends toward lower taxes, lower population density, and high-amenity areas such as Florida, South Carolina, and Idaho. People moving to Montana also typify those preferences and bring higher incomes, often prioritizing lifestyle over affordability constraints. With two-thirds of states having higher median incomes, it’s expected that many of these out-of-state households have greater financial means than local wage earners. If the recent migration patterns continue, Montana’s housing market will remain at least warm, driven by the steady domestic demand.

Interest rates, continuing to be higher than in recent memory, have dominated this year, effectively freezing activity for many buyers and sellers. First-time buyers and local wage earners who rely on financing have left the market. Sellers, too, face difficult decisions, as moving means entering a market with higher interest rates and higher per-square-foot prices than the homes they would be leaving, often necessitating a smaller or less desirable home. When coupled with 2024’s higher financing costs, the result has been a substantial decline in both home moves and ownership opportunities for low- to middle-income earners, including first-time homebuyers.

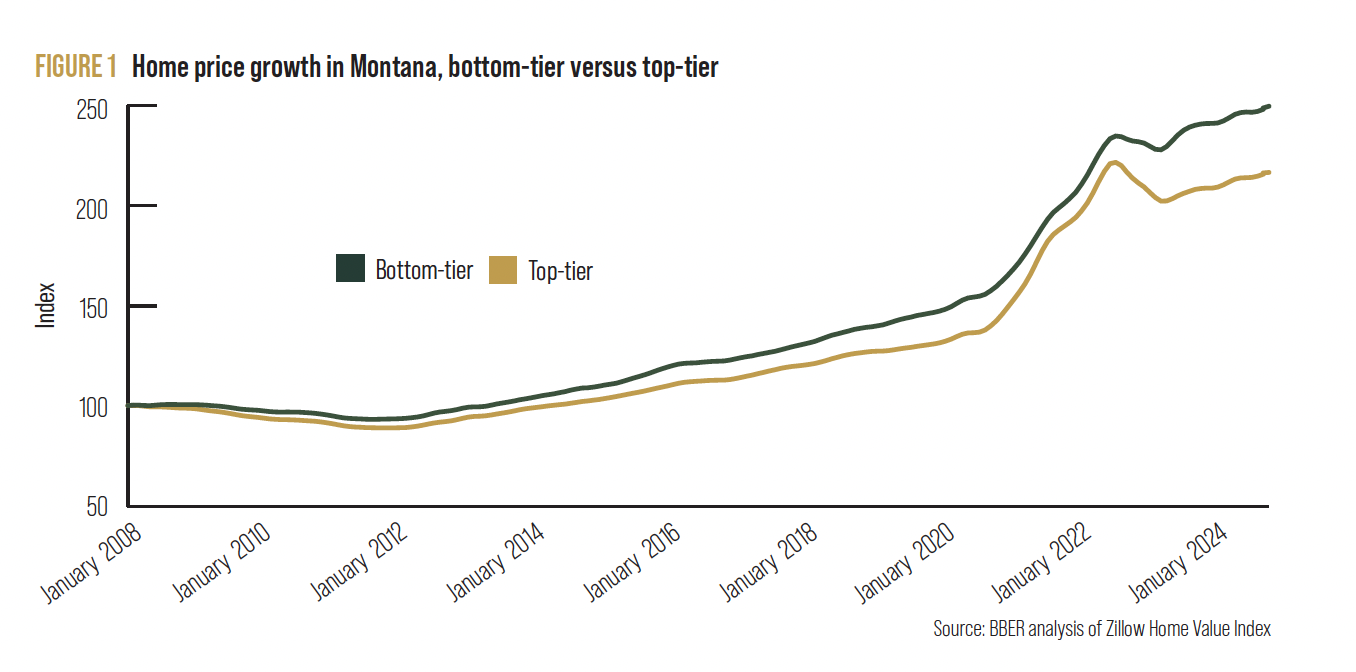

Despite this freeze in both supply and demand, home prices have continued to rise overall, but not equally across price points. Figure 1 illustrates how home price appreciation in Montana has varied between the bottom and top thirds of the market since the Great Recession. While the bottom-tier homes have appreciated faster than the top-tier homes, the gap between the two widened significantly after the market peaked in September 2022. By October 2024, this difference had grown to 33 points, meaning that lower-priced homes have increased in value 33% more than higher-priced homes since January 2008. Before the pandemic, in January 2020, the difference between the indices for bottom-tier and top-tier homes was approximately 16 points. This growing gap reflects the continued pressure on the lower end of the market as household budgets push buyers toward the bottom tier while demand for higher-tier homes stabilizes.

Despite this freeze in both supply and demand, home prices have continued to rise overall, but not equally across price points.

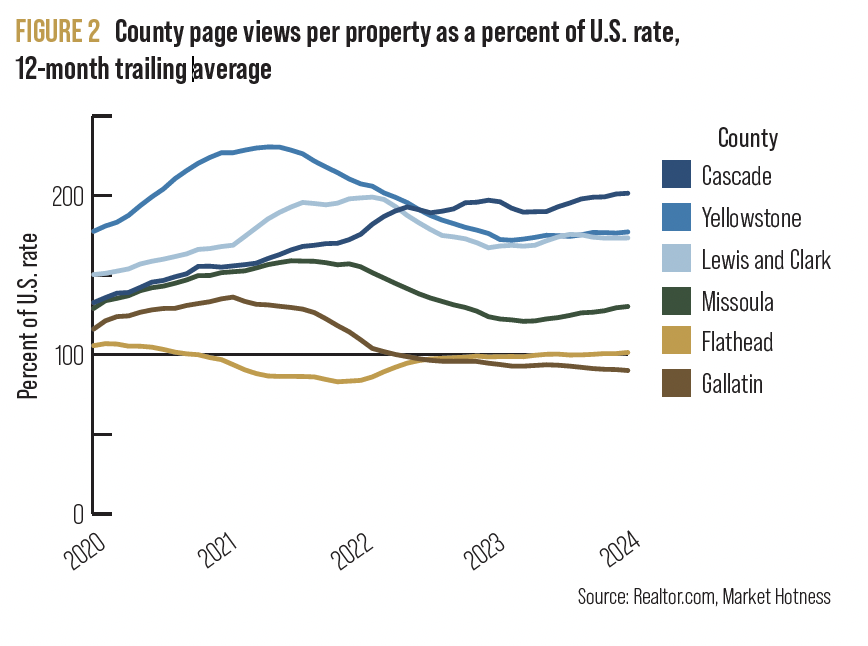

On a broader scale, demand in Montana has begun to shift across different parts of the state. Traditionally the “hottest” markets, such as the areas surrounding Bozeman, Kalispell, Whitefish, and Missoula, are seeing a cooling in demand as buyers increasingly turn to relatively lower amenities but also lower costs, including Great Falls, Billings, and Helena. Similarly to the shift toward lower-tier properties within the market, higher relative prices in these high-amenity areas are nudging buyers to seek affordability in less competitive parts of the state.

Figure 2 highlights this shift, showing the ratio of unique views per property on Realtor.com in various Montana communities compared to the national average. A ratio of 1 indicates that a property in the respective market receives as much attention as the typical U.S. property. While Gallatin and Flathead counties — long the hottest corners of the state — now attract attention more in line with the rest of the country, areas like Great Falls, Billings, and Helena are drawing between 0.75 and 1 additional views per property compared to the U.S. average. This trend suggests a reshuffling of desirability, as affordability constraints and the higher relative prices in high-amenity markets drive buyers toward more affordable parts of the state.

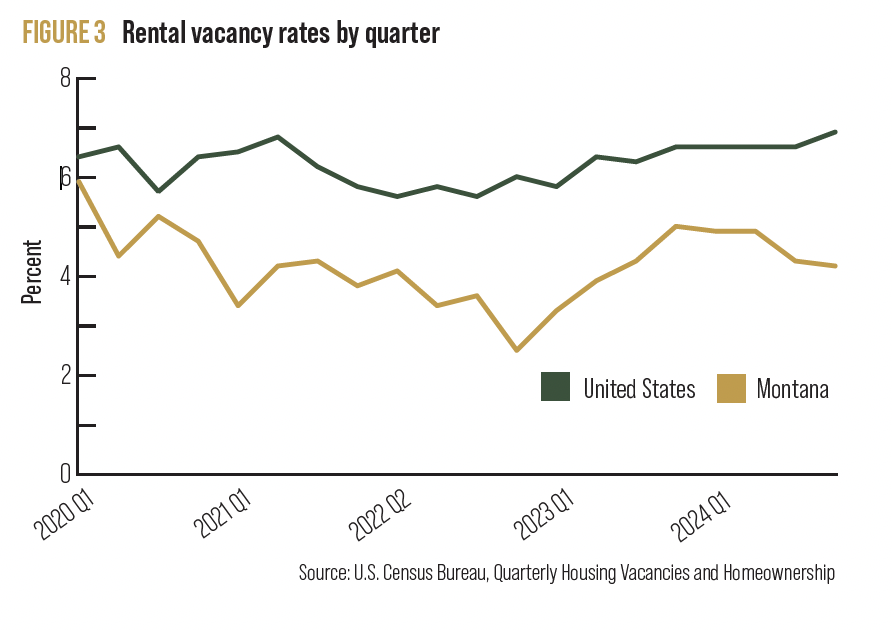

The shift in demand across different scales of Montana’s real estate market — between price tiers and across geographic regions — reflects the broader adjustments buyers are making in response to affordability challenges. As these patterns unfold, they reveal not only the pressures homebuyers face but also the potential for relief in other parts of the market. One such point of optimism lies in the state’s rental market, where rising vacancy rates suggest that the multi-family housing boom in Montana’s cities may be providing critical relief for the working-class population.

Figure 3 highlights a recent uptick in rental vacancies across Montana following the rest of the country, offering much-needed relief from the extreme market tightness experienced just two years ago.

This easing can be attributed to a wave of multi-family construction initiated in 2021 and 2022, which added over 8,000 units statewide during that period. While the pace of new construction has since slowed, these additional units have contributed to cooling down the rental market. Vacancy rates have risen from a historically low 2.5% in late 2022 to a still tight but healthier 4.2% in 2024. These developments indicate that, while affordability challenges persist, the rental market is showing signs of rebalancing, offering critical breathing room for Montana’s renters.

As 2024 ends, Montana’s real estate market reflects both cooling trends and persistent pressures. The Federal Reserve’s recent decision to lower interest rates to 4.5%-4.75% signals cautious economic adjustments. However, the Fed’s measured approach — leaving room for pauses or further cuts — suggests affordability challenges could persist into 2025.

Meanwhile, broader market shifts, like the high-profile settlement against the National Association of Realtors (NAR) regarding real estate commisions and declining membership due to poor market conditions, reveal how external pressures reshape the real estate industry. Additionally, commercial real estate uncertainties, such as rising office vacancies and underperforming retail spaces, compound economic risks. These issues will remain a focus for the Bureau of Business and Economic Research in the coming year.

Yet, the broader climate remains warm, fueled by both in-state and out-of-state demand, along with the gradual but impactful forces of demographics. Montana has one of the oldest populations in the West, but this is slowly changing as younger households and working-age individuals are increasingly drawn to — or are returning to — the state. This demographic evolution, coupled with sustained demand, continues to drive housing pressures, particularly in the lower-tier segment. Without sufficient development to meet this growing demand, affordability challenges will persist, cascading down the price scale. While the cooler conditions of 2024 have offered some relief, they are unlikely to fundamentally reshape Montana’s long-term housing dynamics. The state’s market remains defined by persistent underlying warmth, even as temporary cold fronts pass through.

Derek Sheehan is an economist at the Bureau of Business and Economic Research at the University of Montana.